Medicare

What Is Original Medicare?

Original Medicare is the traditional government-run health insurance program made up of two parts:

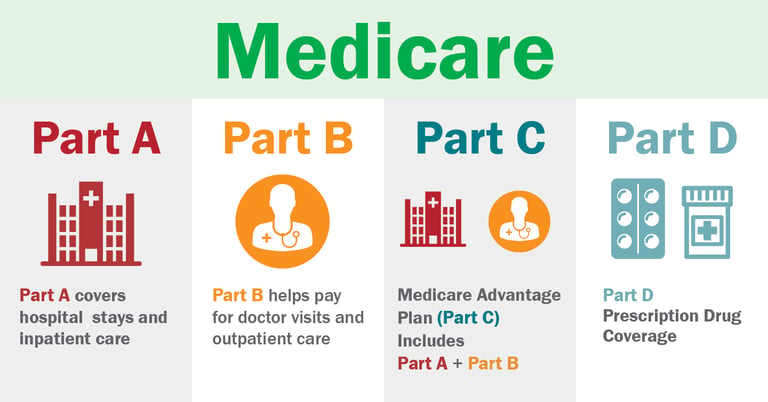

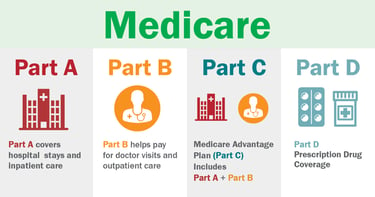

Part A – Hospital Insurance

Part B – Medical Insurance

Together, they cover a range of services, such as preventive care, treatment for conditions when needed and support for overall health.

What Original Medicare Does Not Cover

Original Medicare doesn’t cover everything.

Here are some common exclusions:

Prescription drugs (you’ll need Part D or a Medicare Advantage plan)

Routine dental, vision and hearing care

Long-term custodial care (e.g., assisted living)

Cosmetic surgery

Routine physical exams (Medicare covers an annual “Wellness” visit instead)

Part A: What Does It Cover?

Part A is your hospital insurance.

It typically covers the following:

Inpatient hospital stays

Skilled nursing facility care (short-term)

Inpatient care in a nursing home (not long-term custodial care)

Hospice care

Some home health care services

Most people don’t pay a premium for Part A if they or their spouse paid Medicare taxes while working.

How and When to Enroll in Original Medicare

Most people become eligible for Medicare at age 65. Your Initial Enrollment Period (IEP) is a seven-month window that begins the three months before your 65th birthday, includes your birthday month and ends three months after.

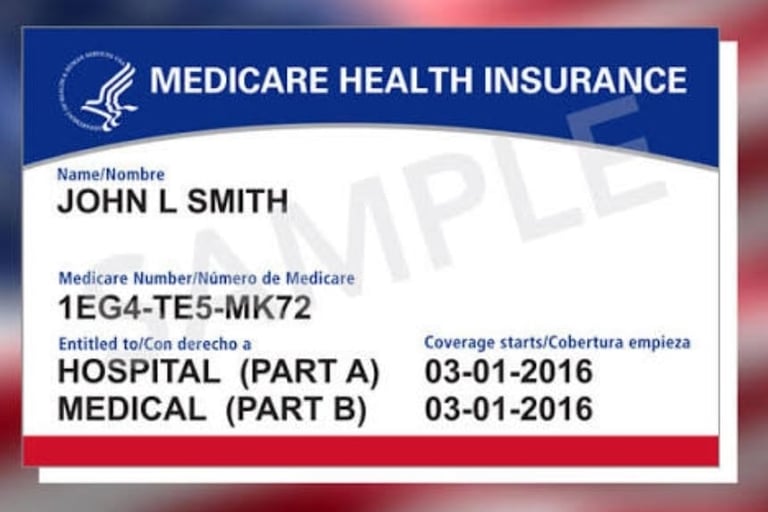

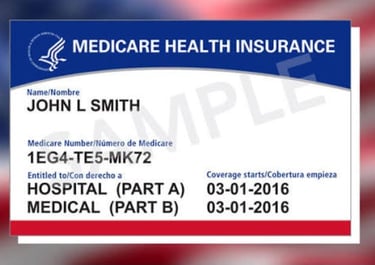

If you’re already receiving Social Security benefits, you’ll be enrolled automatically. Otherwise, you’ll need to sign up through the Social Security Administration.

Once enrolled, you’ll receive your red, white and blue Medicare card in the mail. You can also check your enrollment status online.

Part B: What Does It Cover?

Part B is your medical insurance.

It helps pay for the following:

Doctor visits and outpatient care

Preventive services like screenings, vaccines and counseling

Lab tests, X-rays and diagnostic services

Emergency ambulance transportation

Durable medical equipment, like walkers, wheelchairs, and oxygen

Certain outpatient medications (e.g., chemotherapy, injections)

You’ll typically pay a monthly premium for Part B, along with deductibles and coinsurance.

Part C: Medicare Advantage

Private insurers offer Medicare Advantage plans and include the following:

All benefits of Parts A and B

Usually includes Part D (prescription drug coverage)

Often offer extra benefits like dental, vision, hearing and transportation

Many plans have $0 monthly premiums

Understanding Medicare Part D (Prescription Drug Coverage)

If you don’t choose a Medicare Advantage plan with drug coverage, you can enroll in a standalone Part D plan. These plans cover a range of generic and brand-name drugs, mail-order options for home delivery and offer preferred pharmacies for lower costs.

Medicare is a federal health insurance program primarily for people age 65 and older, as well as some younger individuals with disabilities or specific medical conditions. It helps cover essential health care services such as hospital stays, doctor visits, and prescription medications.

Understanding what Medicare covers — and what it doesn’t — can help you make confident, informed decisions about your health care needs

Part D Coverage Stages:

Deductible Stage: You pay 100% until your deductible is met

Initial Coverage: You and your plan share costs

Coverage Gap (“Donut Hole”): You pay up to 25% of drug costs

Catastrophic Coverage: You pay a small copay or 5% of drug costs

Medicare Supplements Plan

Medicare supplement plans, also known as Medigap plans, are standardized policies sold by private insurance companies to help pay for some of the out-of-pocket costs that Original Medicare (Part A and Part B) does not cover. The plans are identified by letters (A, B, D, G, K, L, M, and N are generally available for new enrollees), and the benefits for each lettered plan are identical across all insurance companies.

Popular Medigap Plans

The right Medigap plan depends on your health needs, budget, and location. Two of the most popular options for new Medicare enrollees are Plan G and Plan N.

Plan G

Plan G is one of the most comprehensive Medigap plans available to new Medicare beneficiaries. It covers most Medicare-approved out-of-pocket expenses after you meet the Part B deductible, providing strong and predictable coverage.

Plan N

Plan N typically offers a lower monthly premium compared to Plan G. It covers most Medicare Part B coinsurance, with small copayments for certain office and emergency room visits. This plan does not cover Part B excess charges.

AGMF INSURANCE LLC

Villa Rica, GA 30180